Half Yearly Assessment of Bangladesh Economy

The Unnayan Onneshan (UO), in its current issue of Bangladesh Economic Update aims at carrying out half yearly assessment of the economy for FY 2014-15 against the backdrop of current economic management by the new government of which 154 members of parliament get unelected in the national parliament election of 2014 which is widely questioned because of its quality of not being participatory as country’s one of the largest political parties did not take part in the election. Following a rigorous scrutiny of the major macroeconomic indicators, the Update puts forward a seven-point policy measure as well as a particular call for an inclusive political dialogue that reducing the exigencies of current political uncertainly will ensure consolidation of democracy through regular transfer of power and cause the economy to grow faster.

The Unnayan Onneshan (UO), in its current issue of Bangladesh Economic Update aims at carrying out half yearly assessment of the economy for FY 2014-15 against the backdrop of current economic management by the new government of which 154 members of parliament get unelected in the national parliament election of 2014 which is widely questioned because of its quality of not being participatory as country’s one of the largest political parties did not take part in the election. Following a rigorous scrutiny of the major macroeconomic indicators, the Update puts forward a seven-point policy measure as well as a particular call for an inclusive political dialogue that reducing the exigencies of current political uncertainly will ensure consolidation of democracy through regular transfer of power and cause the economy to grow faster.

The Update reveals that the rate of growth in gross domestic product (GDP) may fall short of the target of 7.3 percent in FY 2014-15 due mainly to increasing savings-investment gap, unsatisfactory collection of revenue vis-à-vis target, declining rate of growth in agriculture and manufacture, disarrays in external balance, infrastructural underdevelopments, institutional weaknesses and political uncertainties.

Considering the historical trend of the rate of growth in GDP and assuming the same business scenario, the Unnayan Onneshan projects that the rate of growth in FY 2014-15 is likely to fall below the target of 7.3 percent set in the annual budget, thereby remaining under seven percent for the next fiscal year against the target of a rate of growth of eight percent in FY 2016-17. Stagnant investment together with low rate of ADP implementation and shortfall of revenue is impeding the expected rate of growth in GDP. Besides, large trade deficit, underdeveloped infrastructure and crisis in banking sector have been exerting adverse effect on the economy causing the rate of growth to decelerate.

Ambitious fiscal targets, both from income and expenditure sides, set for FY 2013-14, did not materialise at the end of the fiscal year, although the government has been struggling to boost up its revenue earning. Several issues like narrow tax base, concentrated tax sources and tax evasion as well as tax avoidance are causing the collection of revenue to fall below the target. The current status of revenue collection, however, implies that the target that was set in annual budget might be not achieved at the end of FY 2014-15. The allocation of Annual Development Programme (ADP) has been continuously increasing over the last twenty years, whereas implementation has been consistently falling far short of targets.

External sector is undergoing an unsatisfactory performance due mainly to recent decrease in the surplus in current account, which may threaten to exert pressure on country’s balance of payments. In the first quarter of FY 2014-15, the economy experienced deficit in current account balance due to increase in import, decrease in export and foreign aid disbursement, although an increase in portfolio investment keeps the overall balance positive.

Country’s banking sector being characterised by high rate of interest, excess liquidity and declining growth in disbursement of credit to private sector, intermediating lower investment, coupled with poor risk management, fraudulence, driven by captured governance and lax oversight, resulting in lower profitability to the shareholders is caught in trap. Besides this backdrop, questions are being raised concerning the far- sighted deregulation of the financial sector.

Finally, poor energy infrastructure and underdevelopment in road and transportation system are directly related to below the target performance of the economy and cause the rate of growth to slow down. Large amount of investment and good governance are, however, needed in order to improve the infrastructure to ensure sustainable path of economic growth.

- GROWTH, SAVINGS AND INVESTMENT

The Growth Scenario

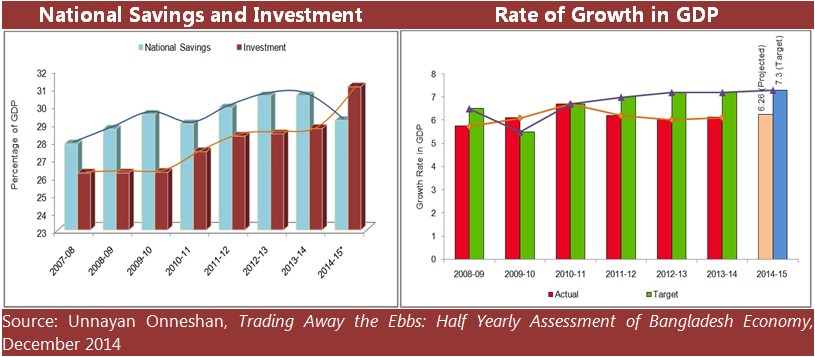

The target of rate of growth has been being set over seven percent in recent years, whereas the actual has been sticking to around six percent. The slow rate of growth in GDP can however be ascribed to mainly three issues – stagnant private investment, shortfall in revenue collection and low implementation of ADP along with lack of infrastructural developments.

The GDP is growing at a decelerating rate. In FY 2011-12, the rate of growth in GDP was 6.52 percent where it became 6.01 and 6.12 percent in FY 2012-13 and FY 2013-14 implying a decrease by 0.4 percentage point from FY 2011-12 to FY 2013-

- 14. During these periods, the targeted rates of growth, however, were 7 percent, 2 percent and 7.3 percent respectively. So the difference between the actual and target is quite clear. Taking the account of the trends of growth from FY 2005-06, the rate of growth is projected to be 6.16 percent and 6.23 percent in FY 2014-15 and 2015-16 respectively.

Figure 1: Actual Growth in GDP and Projection

Source:Ministry of finance,2014

Not only in the budget but also in the MTTF for 2015-17, projection of rate of growth diverges from real situation. A great mismatch exists between the projection and actual rate of growth by MTMF which has been revised five times during the regime of current government.

Table 1: Projection of MTMF and actual rate of growth

| Compo nent | MTMF | 2008-

09 |

2009-

10 |

2010-

11 |

2011-

12 |

2012-

13 |

2013-

14 |

2014-

15 |

2015-

16 |

|

GDP Growth |

MTMF 08-11 | 6.5 | 7.0 | 7.2 | |||||

| MTMF 09-12 | |||||||||

| 5.5 | 6.0 | 6.5 | |||||||

| MTMF 12-16 | 6.7 | 7.0 | 7.2 | 7.6 | 8 | ||||

| MTMF 13-17 | |||||||||

| 7.0 | 7.2 | 7.6 | 8 | ||||||

| MTMF 15-17 | 7.2 | 7.3 | 7.6 | ||||||

| Actual Growth in GDP | |||||||||

| 5.74 | 6.07 | 6.71 | 6.23 | 6.03 | 6.12 | ||||

Source: Ministry of Finance,2014

In FY 2013-14, the actual growth in GDP was 6.12 percent against the MTMF target of 7 percent. In FY 2012-13 the target was 7 percent where the actual rate of growth was 6.03 percent implying 1.17 percentage point gap between the actual and the target. In the sixth fiscal year of the present government (FY 2014-15), the MTMF targeted rate of growth in GDP is 7.3 percent (one percentage point higher than the previous fiscal year) and 7.6 percent in FY 2015-16. Considering the current performance of the major indicators of the economy, projection shows that the government could not achieve its growth target in current fiscal year.

Figure 2: Comparison of real GDP growth projected by MTMF and UO

Source: Author’s calculation

- Savings and Investment

In an economy, savings and investment provide the most important economic link between the past, the present, and the future (Mukharji and Chowdhury, 2013). An adequate rate of national savings is essential to achieving higher investment and consequently higher economic growth. Of late, the rate of growth in GDP has been constrained as investment especially the private investment has not been increasing at a satisfactory rate.

2.2.1 Savings-Investment Gap

The rate of savings and investment to the GDP has remained sluggish over the years and the gap between savings and investment has assumed an increasing trend lately, suggesting that the government’s macroeconomic strategies fall short of converting the savings into investment. In Bangladesh, the gap between savings and investment prevails for a long time. In 2012-13 and 2013-14, the national savings were 30.53 percent and 30.54 percent respectively, whereas the investments were

28.39 percent and 28.69 percent of the GDP respectively, representing 2.14 and 1.85 percentage point gaps between savings and investment. The private investment has been declining since FY 2011-12, although the public investment has been increasing. High interest rate, lack of available supply of electricity and gas, and political uncertainty in the country are causing the private investment to decline. In 2011-12, the private investment was 22.50 percent of GDP which reached

21.75 percent and 21.39 percent in 2012-13 and 2013-14 respectively.

Along the trend of savings and investment since FY 2007-08, the national savings might be 31.04 percent and 31.53 percent of the nominal GDP in FY 2014-15 and FY 2015-16 respectively and total investment might be 29.15 and 29.60 percent of the nominal GDP in 2014-15 and FY 2015-16 respectively. The savings-investment gap has increased sharply compared to the 2010-11 and it will continue further, if the existing policies prevail in future. The saving –investment gap might reach 1.89 percent and 1.92 percent of the nominal GDP in FY 2014-15 and FY 2015-16 respectively.

Figure 3: Savings- Investment gap

Source: Bangladesh Bank and Finance Division, Ministry of Finance, Bangladesh, 2014

- REVENUE- EXPENDITURE BALANCE

The gap between expenditure and revenue has been increasing on a year-to-year basis. The revenue collection does not live up to the expectation. As a result, the government cannot finance all of the expenditures and has to borrow from both external and domestic sources to finance the expenditure, causing non- development expenditure to increase and thus development expenditure to decrease.

- Revenue Balance

From the historical trend, it is seen that the target and actual collection of revenue do not match. Revenue scenario is generally reflected by the tax–GDP ratio, tax base, and the success or failure of the revenue collection. Lower revenue collection-induced failure at achieving the targets of revenue collection therefore shrinks the ability of the government to channel adequate resources to expand productive capacity and to allocate sufficiently for social sector and infrastructure.

- Tax GDP ratio

Tax–GDP ratio of a country shows the financial capability of the government to finance its expenditure. Low tax–GDP ratio implies stringent financial constraint for the government which shrunken the capital expenditure. The tax-GDP ratio is very low with about 10 percent of the GDP in Bangladesh, but keeps improving at a slow pace. Low per capita income, corruption and inefficiency in tax management system keep the tax collection low and unsatisfactory. To increase the contribution of tax in GDP the collection of tax must be accelerated through proper management in tax collection and tax policy reform. In FY 2013-14, the tax was 9.6 percent of GDP where the target was set to 11 percent in MTTF; 1.4 percentage point less than the target. In current fiscal year, the target for Tax-GDP ratio is 11.6 percent. Taking account of the annual rate of growth in tax-GDP ratio from FY 2005-06 to FY 2013-14, it is projected that the Tax-GDP ratio might be 9.94 percent and 10.27 percent in FY 2014-15 and 2015-16 respectively.

Figure 4: Tax-GDP ratio (actual and target)

Source: Ministry of Finance, 2014

But the status of Tax-GDP ratio is the worst among the SAARC countries except Afganistan. Both Tax-GDP ratio and revenue- GDP ratio are the lowest in Bangladesh among the seven SAARC countries. Even Nepal and Srilanka have higher tax- GDP ratio of 13.9 percent and 12 percent respectively in 2013. The tax-GDP ratio in India and Pakistan were 10.7 and 10.1 percent, where tax-GDP ratio was 9.7 percent in Bangladesh in 2013.

Figure 5: Comparison with other countries

Source: World Development Indicator,2013

Narrow tax base

The prevalence of narrow tax base is hindering the development of a strong revenue base in the country. Tax evasion and avoidance, High cost in collecting tax, mismanagement in tax system and lack of incentive to pay tax are narrowing the tax net.According to the National Board of Revenue (NBR), only less than 1% people pay income tax. Income tax is the largest source of direct tax. But the contribution of income tax in total tax is not satisfactory. With the population of 15.58 crore, the total number of the holders of Taxpayers Identification Number (TIN) is only 17 lakh (1.09 percent of total population), of which only 8.55 lakh (0.54 percent of the total population) submitted their tax returns in November 2014. The number of eligible tax payers is 69 lakh whose monthly income ranges from Tk. 20000 to Tk. 35000+. This statistics implies that only 4.43 percent of total population has taxable income, although they are not paying tax.

- Revenue collection

In the July-October period of the FY 2014-15 the total revenue collection is Tk. Tk.38005.81 crore where the target is Tk.149720 crore, that is 25 percent of the target is collected. In 2013-14 and 2012-13, 96 percent and 97 percent of the target was collected respectively. In FY 2013-14, the target of revenue collection was Tk. 130178 crore and the actual collection was Tk. 125125.47 crore – a shortfall of Tk. 5052.3 crore. In FY 2012-13, the target was set to 116824 core, where the actual collection was 113271.31 crore – a shortfall of 3552.3 crore. In FY 2013-14, the shortfall in revenue collection than the target increased by 42.22 percent.

From these historical trends, in the current fiscal year the target of revenue collection might not be achieved.

Figure 6: Target and actual collection of revenue

Source: Bangladesh Bank, 2014

Several issues have gained importance in recent times. The first concern is the prevalence of narrow tax net, which acts as a hindrance to having a stronger revenue base in the country. The second important concern includes the issue of tax burden and tax incidence. Although the government is putting emphasis on direct tax i.e. income tax, the revenue collection of the country largely depends on the indirect taxes i.e. VAT. Thirdly, in FY 2012-13, both NBR and non-NBR taxes have failed to satisfy the target of revenue collection with total shortage of Tk. 3552.7 million.

Income tax has been determined on five slabs progressively with income level. But when the collection of VAT is considered with direct tax, the higher burden of tax on marginalized group seems apparent. Moreover, certain types of taxes such as the inheritance tax are absent in Bangladesh which could be supportive to enhance the tax base.

In addition, capital flight is also responsible for the low revenue income in Bangladesh. The amount of money flown out of Bangladesh through illicit means tripled in 2012 to stand at USD 1.78 billion (stand fourth in South Asia), riding mainly on trade misinvoicing. The figure was USD 593 million the year before. Use of hundi, misinvoicing in export and import, illegal money through tax evasion are the facets of capital flight. This unaccounted transfer of money is a big blow for the economy as it means lost investments and revenue income for the government.

NBR and non-NBR Tax

Total revenue is collected either from tax or from nontax sources. In total revenue, tax revenue moved 80.9 percent to 83.09 percent between FY 2007-08 and FY 2013-14. Of the total tax revenue, nearly 95-96 percent is collected by the NBR. In FY 2013-14, NBR collected Tk. 16657.18 crore which is 10.46 percent higher than that of previous year. The amount of tax from non –NBR sources was TK. 4612.64 core which is 11.75 percent higher than that of the previous year. During the July- October period of FY 2014-15, NBR collected Tk. 38005 crore (25 percent of the target) which is 14.24 percent higher than that of the same period of the previous fiscal year.

In FY 2014-15, actual revenue collection is Tk. 38005.81 crore (till October, 2014), which is only 25.38 percent of the target of Tk. 149720 crore for the whole year. Among the main sources of revenue in FY 2014-15, NBR revenue from income tax, VAT, and custom duties is targeted at Tk. 56086 crore, Tk.55013 crore and Tk. 15874 crore respectively, whereas actual revenue collected till October, 2014 is Tk. 11678.51 crore (21 percent), Tk. 14938.82 (27.16 percent) crore and Tk. 4608.47 (29.08 percent) crore respectively.

Table 2: Target, Actual and Projection

| 2013-14 (tk. million) | First Quarter of 2014-15 (July- September) | ||||||

| Particulars | Target | Realisation | Gap Between target and Realisation | Percentage Change from previous year | Target | Realisation (Tk. million) | Percentage Change from corresponding period of 2014-

15 |

| VAT | 49556 | 44571.01 | 4985 | (+8.15) | 55013 | 14938.8

2 |

(+14.99) |

| Custom duties | 15984 | 13540.82 | 2443.18 | (+1.64) | 15874 | 4608.47 | (+1.64) |

| Income Tax | 48297 | 42915.50 | 5381.5 | (+15.61) | 56086 | 11678.51 | (+13.66) |

| Total NBR Tax | 136090 | 120512.8

3 |

15577 | 10.41 | 149720 | 38005.8

1 |

(+14.24) |

| Non- NBR Tax | 5129 | 4612.64 | 516.36 | 11.75 | 5572 | 380.55(

Sep) |

— |

Source:Bangladesh Bank,2014

3.2 Expenditure and Deficit

The gap between total expenditure and total revenue is getting bigger over the years due to low collection of revenue, causing fiscal deficit-induced macroeconomic underperformance and higher non-development expenditure. The overall budget deficit for FY 2014-15 is estimated at Tk. 67552 crore that represents 5 percent of GDP. The revised deficit in FY 2013-14 was Tk. 59551 crore (5 percent of GDP), which was Tk. 55,032 crore (4.6 percent of GDP) in the proposed budget. Since the revenue collection target of the government seems to be ambitious, the government may be forced to cut the expenditure level in FY 2014-15 to keep the budget deficit within the target. The three fiscal targets related to revenue earning, revenue expenditure and budget deficit thus has not been achieved and the government had to revise these by a significant margin.

Figure 7: Budget Deficit

Source:Budget in Brief,2014

3.2.1 Component of expenditure: development and non- development

Both development and non development expenditure are increasing in terms of absolute amount, but the rate of growth in non-development expenditure is higher than that of development expenditure. The rate of growth in non- development expenditure has increased to 20.39 percent in FY 2013-14 from 10.56 percent in FY 2012-13, the rate of growth in development expenditure has decreased to 8.33 percent in FY 2013-14 from 31.73 percent in FY 2012-13. The non development expenditure is much higher than the development expenditure. In 2012-13 and 2013-14, the non development budget were 12.1 percent and 13.2 percent of total GDP, where the ADP was only 4.7 percent and 5.1 percent respectively during the same time periods. In FY 2014-15, the allocation for the non development expenditure and ADP expenditure is 12.7 percent and only 6.3 percent of the total GDP respectively. Increasing allocation for non-development expenditure due to financing the deficit does not allow the government to allocate adequately for development expenditure resulting in barrier to the expansion of productive capacity in the economy.

| Figure 8: The rate of growth in development and non development expenditure | Figure 9: Ratio of ADP and non development expenditure |

Source: Ministry of Finance, 2014

- Deficit financing instrument: Debt

The mismatch between the revenue and expenditure is fulfilled by borrowing both from domestic and external sources. In the first quarter of the current fiscal year (July-October’14), the deficit financing increased by three times than the same time period of the previous year. In July – October period of FY2014-15, the deficit financing is Tk.12060.15 crore where it was Tk.4476 core in July-September of FY2013-14. The borrowing from domestic sources has increased more than that from external sources. In the July –September period of FY2014-15, financing from external sources is Tk.1140.51 crore and from domestic sources is Tk.10919.64 crore. Among the domestic sources, borrowing from the banking system does not increase much, whereas the borrowing from the non banking sources has increased drastically specially from selling the NSD certificates. Government plans to collect Tk. 9056 crore through NSD certificate in FY 2014-15, but in first five

months of this fiscal year, NSD certificates with the value of Tk. 9677 crore have been sold which is 206.31 percent higher than that of same time period of the previous year and Tk. 621 crore higher than the target.

Figure 10: Sale of NSD certificate

Source: Bangladesh bank, 2014

- Per capita debt burden

In FY 2013-14, the per capita debt burden was Tk. 12968 and per capita external debt was USD149.2. Projection says that the per capita domestic debt will be Tk.15969.42 and Tk. 18970.5 in FY 2014-15 and FY 2015-16 respectively and the per capita external debt might be USD 153 and USD 158 during the same periods of time.

Figure 11: Per capita external debt

Source: Bangladesh Bank,2014

- Cost of debt: Principal and interest

Every year government has to pay a huge amount of principal and interest. Interest payment is the largest portion of non- development expenditure. In 2014-15, 12.4 percent of total budget expenditure is allocated to pay the interest of domestic and external debt, whereas the allocation was 12.5 percent in 2013-14. During the same time (FY 2014-15), the allocations for education, health and housing were 13.1 percent, 4.4 percent and 1.8 percent respectively.

Table 3: Budgetary allocation on different sector (In percent)

Source: Budget in Brief, 2014-15, 2013-14 and 2012-13

- ANNUAL DEVELOPMENT PROGRAMME (ADP)

Every year, the government sets a highly ambitious ADP target which is unrealistic in view of low implementation capacity. ADP allocation has been increasing continuously over the last twenty years (except FY 2008-09), but implementation has been consistently falling short of target, causing the economy to undergo decelerations in recent years. Moreover, it is observed that the rate of increase in ADP implementation has been decreasing. In FY 2012-13, 96 percent of total ADP was spent, whereas it stood at 94 percent in FY 2013-14, implying 2 percentage points decrease in ADP implementation. Allocation for ADP in the current fiscal year (FY 2014-15) is Tk. 80315 crore, 33.85 percent higher than that of the revised ADP of the last fiscal year (FY 2013-14). ADP implementation in October 2014 was Tk. 11250.82 crore (13%) which is 8.52 percent higher than that of the corresponding month of FY 2013-14. ADP implementation up to October of the current fiscal was higher than in any of the last five fiscal years.

Among the ministries/divisions, ministry of primary and mass education implemented highest amount of ADP allocation (23percent) and ministry of housing and public works implemented the lowest (4 percent). Furthermore, the average implementation as percentage of revised ADP was 91.12 percent during FY 2009-10 – FY 2012-13, whereas it was 90.23 percent during FY 2000-01 – FY 2005-06. In 2013-14, 94 percent of total ADP was implemented. An estimate based on past data reveals that total implementation as percentage of proposed ADP might reach 94.27 percent by the end of FY 2013-14.

Table 4: ADP Implementation

| Year | Allocation (in crore) | Expenditure (in crore) | %share of implementation |

| 2004-05 | 20500 | 18771 | 91.6 |

| 2005-06 | 21500 | 19473 | 91 |

| 2006-07 | 21600 | 17917 | 83 |

| 2007-08 | 22500 | 18850 | 83.8 |

| 2008-09 | 23000 | 19688 | 85.5 |

| 2009-10 | 28500 | 25917 | 91 |

| 2010-11 | 35880 | 32854 | 92 |

| 2011-12 | 41080 | 38020 | 93 |

| 2012-13 | 52366 | 50035 | 96 |

| 2013-14 | 60000 | 6370523 | 94 |

| 2014-15 | 86000 | 11250(July-Oct’14) | 13 |

Source: Internal Monitoring Division, Ministry of Planning,2014

- EXTERNAL BALANCE

A deceleration in the growth of export earnings coupled with declining growth in the export of readymade garments has been observed of late signaling a state of economic exigencies. External sector is undergoing this unsatisfactory performance due mainly to recent decrease in the surplus in current account, which may threaten to exert pressure on country’s balance of payments. In the first quarter of FY 2014-15, the economy experienced deficit in current account balance due to increase in import and decrease in export, deficit in service account and decrease in foreign aid disbursement. On the other hand, an increase in portfolio investment, however, keeps the overall balance positive.

5.1 Trade Balance

Between July and September of the current fiscal year, trade deficit was USD 1128 million which is more than that of the same period of the previous fiscal year. Trade deficit in the first quarter of FY 2014-15 has increased by 17.97 percent because the export earning has decreased by USD 71 million, whereas import payment has increased by USD 1199 million during this period. Export earnings decreased slightly by 0.97 percent during July-October, 2014 (First quarter of FY 2014- 2015). Political turmoil and sluggishness in the industrial production discourage the retailer for importing intermediate goods from this country. Import payments during July- September of 2014 increased by 5.41 percent and stood at USD

10338.20 million against USD 9808.00 million of July- September of 2013. Fresh opening of import LCs during July- September, 2014 increased by 10.92 percent compared to the previous fiscal year and stood at USD 9796.09 million.

- Balance in service

A large imbalance in service sector is prevailing for a long time which remains unnoticeable. The components of service sector are intangible which are travel, transportation, commercial services and government services (pocshman and Pelletier, 1999). In FY 2013-14, the gap between the credit and debit was USD 4189 million which was USD 3162 million in FY 2012-13 implying 32.42 percent increases in gap. In the July–September period of FY2014-15, the deficit in service has increased to USD 1333 million which was USD 880 million during the same period of the previous fiscal year. The increasing deficit in service explicates that the economy is not only lagging behind in terms of trade but also in terms of service, which is worsening the balance of payment. Based on the previous it can, however, be projected that the deficit in service account may rise to USD 4959 million in FY 2014-15.

Figure 12: Deficit in service account

Source: Bangladesh Bank, 2014

- Capital machinery import

Imports of capital machinery increased by 124.82 percent in the first quarter of the current fiscal year despite the unsatisfactory investment climate. During July–September of the current fiscal year, USD 691.36 million worth of settlement of letters of credit for capital machinery took place, implying

124.82 percent year-on-year increase, whereas it was about USD 566.54 million in FY 2013-14. The import of capital machineries reached USD 2005 million in FY 2011-12 and then came down to USD 1835 million in FY 2012-13 and stood USD 1392 million during July – January of FY 2013-14. A decline in import of capital machinery implies the lack of entrepreneurship and productive capacity expansion, which together with current unemployment of large productive capacities in manufacturing sector may cause the rate of growth in GDP to decelerate in the current fiscal year.

Remittance

Setting aside the role of remittances in terms of beefing up the foreign exchange reserves and enhancing the ability to import, remittances received from overseas also play a vital role in strengthening consumption of the rural people. In the last fiscal year, the rate of growth in flow of remittance become negative (-1.6percent) for the first time within last ten years, but during July-November of FY 2014-15, remittances went up by 11.54 percent and stood at USD 6204.52 million compared to the same period of the previous year.

The inflow of remittance shows a sluggish increasing rate from FY 2009-10 because of the crisis in Middle Eastern countries and reduction in the demand for labour of Bangladesh from Malaysia, Saudi-Arabia, Kuwait and Singapore. In 2003, Saudi Arabia was the largest market for exporting manpower where 64 percent people of total migrants went to and the number decreases to 4 percent in 2013. In 2003, 15 percent, 10 percent, 3 percent and 2 percent of total migrants destined to UAE, Kuwait, Bahrain and Singapore, whereas the percentage stood at 4 percent, zero percent, 7 percent and 18 percent respectively in 2013. Export of manpower abroad has fallen in especially those traditional markets like Saudi Arabia, Malaysia, and UAE due to lack of proper diplomatic strategies, violation of rules and regulation by the manpower export agencies, illegal entries and increase in illegal activities by Bangladeshies in those countries.

| Figure 13: Countrywise manpower in2003 | Figure 14: countrywise manpower in 2013 |

Source: Ministry of Finance, 2014

- Overall balance

In the July –October period of the current fiscal year, the overall balance of payment has been decreased from USD1649 million toUSD1246 million compared to the same period of the previous FY 2013-14; 32.34 percent decrease in Overall balance. This large decrease is because of increase deficit in trade balance and current account balance.

The current account balance has stood at USD -1261 million in FY 2014-15(July-October)from USD 793 million in FY 2013- 14(July-October) that is the balance decreased by 59.02 percent. Meanwhile, the total import declined by 11.36 percent

and stood at USD 2770 million in July of FY 2014-15 compared to USD 3125 million in the corresponding month of the FY 2013-14.

On the other hand, the financial account increased to USD 2885 million from USD 30 million, represents a 95.17 percent increase which keep the overall balance positive. Financial account increases owing to slight increase in FDI, large increase in portfolio and other investment. In July-october’15, FDI increases by 5.64 percent, Portfolio investment increased by 100 percent and other investment(Medium and long term loans etc.) in financial account balance increased by 253.32 percent compared to the same time period of the previous fiscal year.

Source: Bangladesh Bank, 2014

- Infrastructure

Poor energy infrastructure together with underdeveloped road and transportation system does not provide the investors with necessary incentives and opportunities to invest in the economy, thereby exerting adverse impact on country’s economic growth.

- Power and energy

By ensuring the food security, alleviating poverty and propelling rate of growth in GDP, power and energy guarantees the inclusive and sustainable development in a country. In developing countries like Bangladesh, low rate of growth in GDP (around five to six percent) is associated with

poor physical infrastructure facilities such as shortage of power and energy supplies.

About 62 percent people have the access to electricity in current year that is 38 percent which indicates 59.204 million people have no access to electricity. Up to April 2012, the 53 percent of total population got the electricity where it was 49 percent and 47 percent in 2011 and 2010 respectively. The per capita consumption of electricity is increasing but low compared to other countries; even if lower than Bhutan or Srilanka. The per capita consumption of electricity was 217 kwh in Bangladesh, whereas the per capita consumption in India, Pakistan, Sri Lanka and Bhutan was 529.1 kwh, 368.38 kwh,

431.44 kwh, and 1619.48 kwh respectively.

Figure 16: The per capita consumption of electricity compared to other countries

Source: CIA World Fact Book, 2013

The real demand for electricity could not be met due to the shortage of available generation capacity. A good number of generation units have become very old and have been operating at a much-reduced capacity. As a result, their reliability and productivity are also poor. Beside this, due to the shortage of gas supply, some power plants are unable to utilise their usual generation capacity. Therefore, there is an increase in the load-shedding over the years. The average maximum demand for electricity was 3970 MW in 2007 which increased to 4833 MW in 2011 (May, 2011) with an average increasing rate of 216 MW per annum. In May 2014 the peak demand increases to 7050 MW which was 6700 MW in 2013.

This increased demand over generation has resulted in increased load shedding (Figure 2). Additionally, the average load shedding increased to 656 MW in 2011 (May, 2011) with an average increasing rate of 35 MW per year starting from 2007. In May 2013, the load shedding increased to 932 MW which has decreased to 670 MW in May 2014. The demand for electricity has been increased with a rate of 5.43 percent per year whereas; the generation of electricity has been increased with a rate of 5.37 percent per year between 2007 and 2011.

Figure 17: Projected demand, supply and loadshedding in electricity.

Source: Bangladesh Power Development Board, 2014

Transport is an important component of economic activity in all countries but especially so in those that are developing. The potential for enhancing economic and social development through improvements in the transport sector are very large indeed.(Mahmood et.al,). Unfortunately, no such vision for transport development exists in Bangladesh. The current disturbing trends in transport development indicate the need for policy directions to make such development environmentally and otherwise sustainable and to create a transport system that can meet the growing demand for transport services which is resulting from increasing economic liberation and external orientation of the economy.

The transport system consists of road , railways and inland waterways. Roads and highways are the most widly used .There is 21454 km road ways in the country among which 17 percent is national ,20 percent is local road and 63 percent is district roads. But the condition of theses road is not good. According to the road transport and highways division’s latest road roughness survey, about 11 per cent of the 21,589.65 km roads and highways under its jurisdiction were in ‘bad to very bad’ category, about 30 per cent were in ‘poor’ category and about 58 per cent were in ‘good to fair’ category. 30 per cent of the highways, 35 per cent of regional highways and around 50 per cent of zila roads were in poor or bad condition.

Bangladesh, as a riverine country with 24,000 km waterways, has a navigable network varying from 5968 km during the monsoon to 3865 km during the dry season. Its inland water transport (IWT) continues to be an important mode of transport not only in the inland movement of freight and passengers but also in the transportation of import and export items through the ports of Chittagong and Mongla. The high degree of penetration of the IWT network provides access to about 25% of the rural household in Bangladesh.

Table 5:Road and transport system in Bangladesh

Source:Ministry of Finance,2014;The New Age,2014;World Bank,2013.

Generally, the development in road and transport need large investment because compared to the other sectors, the infrastructure sector is more capital centric. The proposed allocation in this sector stood at Tk. 24464 crore which represent the 9.5 percent of the total budget expenditure. These are higher than the allocation in the budget of FY 2012-

13 and FY2013-14 by Tk. 11967 crore and Tk. 3840 crore, respectively. Special allocation for the Padma multipurpose Bridge is Tk. 6,852 crore included in infrastructure. In terms of budgetary allocation, although the infrastructure sector has seen one of the highest increases in recent times, the effectiveness of this amount, however, would depend on how the money is capitalised. If the money is used to build new roads, railways, etc, the possibility of a greater fiscal multiplier would be created. Moreover, one flaw in the government’s infrastructure development plan is its reliance the PPP initiative, which has already failed to produce real results.

INSTITUTIONAL BALANCE 1Banking sector

Country’s banking sector has been caught in trap and is characterised by high rate of interest, excess liquidity and declining growth in disbursement of credit to private sector, intermediating lower investment, coupled with poor risk management, fraudulence, driven by captured governance and lax oversight, resulting in lower profitability to the shareholders and institutional weakness in the economy. Besides this backdrop, questions are being raised concerning the far-sighted deregulation of the financial sector.

6.1.1 Risk Management

Risk management is measured by Return on asset(ROA), Return on equity(Roe) and non performing loan.ROA indicates the productivity of the assets i.e. how much income is earned from per unit of assets. According to Basel-II accord, ROA should be more than 1 percent. On the other hand, ROE is another important measure of earning and profitability determination which indicates net income after tax to total equity. In 2013, overall ROA in the banking sector was 0.90 percent whereas it was 0.60 percent in 2012. At the end of FY 2013-14 the performance of banking sector deteriorates. In June of FY 2013-14, the ROA decreased from 0.9 percent to0 .6 percent and ROE decreased from 11.1 percent to 8.4 percent. If these trends continue, overall ROA in the banking sector might be

0.82 percent in 2014. Insignificant profit during this period has occurred due to the worst ratio of ROA scenario in SCBs and DFIs. The position of foreign commercial banks (FCBs) was strong enough over the whole period. The DFIs’ situation is not found better due to the operating loss incurred by Bangladesh Krishi Bank (BKB) and Rajshahi Krishi Unnayan Bank (RAKUB).

Figure 19: Return on equity and Return on asset in the banking sector

Source: Bangladesh Bank,2014

Overall net non performing loan (NPL) increased to 3.9 percent in June 2014 from 3.4 percent in March 2014. At end of March 2014, Net NPL ratios for SCBs and SBs increased from 4.7 percent and 24.2 percent respectively at the end of March 2014 to 7.4 percent and 26.4 percent respectively at the end of June 2014.

Excess of liquidity of the banking sector has been increasing over the months mainly due to a noticeably low level of demand for credits by the private sector. Another reason behind the slow growth of credit is the rigid attitude in giving loans due to a number of scams occurred as well as mismatch between credit and deposit growth. At the end of September 2014, total liquid assets stood at Tk. 226926.43 crore(required liquidity was 73819.04 crore) compared to Tk. 214676.09 crore (required liquidity was Tk. 71278.22 crore) at the end of the June ,2014 which was 174171.33 crore at the end of June 2013.

Scrap in loan

Embezzlement of Hall-mark, Bismillah Group and BASIC bank etc. has become talk of the country in recent times. This loan scrap is alarming for our banking as well as the financial sector (see appendix).

7.1.2 Interest rate spread

To keep the inflation rate low, Bangladesh Bank has been promoted contractionary monetary policy for last three or four years. As a result, the interest rate spread is too high to encourage the investors to borrow. High lending rate depresses the investment by raising the cost of investment. For long time interest rate is too high. According to Taylor rule In Bangladesh the interest rate should be around 9 to 10 percent where the interest rate(lending) is set above 13 percent

.(UO,2014) According to the “Taylor Rule” equation, the policy interest rate should be 9.13 percent (calculated through taking into account government’s GDP projection of 7.3 percent and inflation projection of 7 percent), while it remained nearly

12.60 percent on average during the period of July-October of FY2014-15.

Figure 20: Interest rate spread

Figure: Major Economic Trends, Bangladesh Bank, 2014

REAL SECTOR

As the revenue collection by the government has been falling short of target, resources cannot be channeled adequately to the agriculture sector, which cause the rate of growth in agriculture to decline in recent periods. Along the agriculture sector, the manufacturing sector also assumes a decreasing rate of growth due mainly to increased gap between savings and investment and decreased priv

Agriculture Sector

The contribution of agriculture in GDP is decreasing every year. On the other hand the overall rate of growth in agriculture is also declining .Recent declining trend of growth in agriculture can be attributed to a number of reasons. First, the post-green revolution period has not experienced any breakthrough as regards technological advancement in the country on the one hand, and the poor and marginal farmers who comprise the majority of total farm population cannot afford the high cost of using high input technologies in agriculture on the other. Second, despite higher cropping intensity, the declining trend in the availability of arable land causes the growth in agricultural sector to fall. Third, though the budget allocation in agriculture is increasing, the large portion of this allocation goes for meeting non-development expenditure every year leaving a meager amount for development spending, thus constraining development in the sector. For instance, 85 percent of total agriculture-related budget was allocated for meeting non-development expenditure in FY2009-10, 84 percent in FY2010-11 and 85 percent in FY2011-12. Therefore, in order to raise productivity and profitability, reduce instability, and increase efficiency in resource use, increase of the allocation on the development side is important(UO,2014).

The amount of subsidy to the agriculture sector proposed at Tk. 9000 crore for FY 2014-15, which is Tk. 3000 crore lower than the revised budget for FY 2012-13. This subsidy cut would hurt the agricultural production. Finally, agriculture sector lacks specific proposals in the budget for FY 2013-14 about how to speed up the slow rate of ADP implementation, which is a long characteristic of this sector.

Industry Sector

In contrast to agriculture sector, the Industrial and Economic Services sector has received Tk. 2976 crore in the budget of FY 2014-15. This equals a decrease of Tk. 139crore from the revised budget of the preceding fiscal year. However, like the agriculture sector, the challenge for the industry remains whether this allocated amount would be able to sustain the industrial growth, especially when the sector is burdened with multiple problems. In particular, the requirement of investment is huge to shift the industrial growth to a more sustainable one. Like the other sectors, the slow rate of ADP implementation is a problem for the industrial sector as well. Actually, status of implementation of the ADP in industry sector is one of the worst.

The Quantum Index of Production (QIP) which is used for measuring the production performance of the manufacturing industries shows that for medium to large scale industries, the QIP increased to 228.43 in 2000-01 from 141.80 in 1992-93, whereas the index stood at 157.89 and then reached 205.45 in FY2010-11 and FY 2013-14 respectively. Recent trend of QIP shows that QIP for medium to large scale is increasing at a decreasing rate. In 2010-11 the rate of growth in QIP was 16.95 percent, which decreased to 10.79 in FY 2011-12 percent and slightly increased to 11.59 in 2012-13 percent, but in FY 2013-14 drastically decreased to 5.26 percent. Political unrest, lack of adequate energy and power, insufficient source of fund can be held responsible behind the decelerating rate of growth in QIP for medium to large scale manufacturing in recent years.

Figure 21: The quantum index of manufacturing industries (Medium to large scale industries

Source: Ministry of Finance, 2014

Additionally, The rate of growth in the industrial term loan has been experiencing an irregular movement with negative rate of growth since July- September, 2013. Adequate capital is needed for industrialisation of a country. Loan is one of the most important factors of capital formation, mainly for developing country like Bangladesh.

The disbursement of industrial term loan stood at Tk. 12809crore in the first quarter of the current FY 2014-15, which is the highest among the last five quarters, whereas it was Tk. 8880.9crore in the first quarter of the previous FY 2011-14. In the first quarter of the current FY 2014-15, disbursement of the industrial term loan increased by Tk. 2929 crore compared to the first quarter of the previous FY 2013-14. The rate of growth of the disbursement of the industrial term loan stood negative at 26.81 percent in the third quarter of the FY 2013-14, but had a positive rate of growth of 23.47 percent in the last quarter. If the trend remains as usual, the disbursement might increase at the end of the current fiscal year. The condition of the recovery of the industrial term loan has been improved by insignificant amount since the January- March quarter of the previous FY 2013-14.

Figure 22: Industrial term loan

Source: Bangladesh Bank, 2014

- Poverty and Unemployment

With a rate of growth of 3.88 percent from 1995 to 2010, the size of the total labour force increased to 57.1 million in 2010, implying the availability of once-in-a-lifetime demographic dividend, though the lack of employment opportunities may cause the country not to capitalise on the advantage. Along the exigency of unemployment, continuation of recent decelerated decline in the incidence of poverty may witness a large number of people living below the poverty line in the near future, given the current rate of population growth in the country.

Poverty

Despite considerable thrust on poverty alleviation in all plan documents since the independence of Bangladesh, a significant number of people are still living below the poverty line. The rate of unemployment in the country, particularly youth unemployment is rising at a significant rate. The proportion of poor in the population declined considerably between 2000 and 2010. The incidence of poverty decreased from 49.8 percent in 2000 to 40 percent in 2005 and then further to 31.5 percent in 2010 (UO, 2014).Recently world bank estimated that the current poverty rate is 25.6 percent (The Daily Prothom- Alo, 2014). That is the poverty is decreasing at a decelerating rate.From 2000 to 2005 the poverty decreased by 9.8 percentage point where from 2005 to 2010 the poverty rate decreased by 8.5 percentage point .

Unemployment

With a rate of growth of 3.88 percent (from 1995-96 to 2010), the number of total civilian labour force in 2010 increased to

57.1 million. In 1995-96, total civilian labour force was 36.1 million out of which 30.7 million was male and only 5.4 million was female. Out of total civilian labour force, 40.2 million was male and rest 16.9 million was female. A total of 34.8 million were employed and 1.4 million were unemployed in 1995-96, which increased to 54.5 million and 2.6 million respectively in 2010 (BBS, 2011).

When underemployment is taken into account in assessing the status of the labor force in Bangladesh, the perception of the labor market significantly changes. The information on hours worked shows that a total of 10.99 million (which is about

20.31 percent of the employed labor of 54.1 million) were underemployed in 2010. This shows an extremely high level in the number of the people who work less than 35 hours per week.

Also the information shows high incidence of underemployment in rural areas and among the female labor force (Saleh, 2014).

- CONCLUSIONS

Based on the five months’ performance of the economy in the current fiscal year it can be said the major targets of the government described in MTTF and national budget remain unfulfilled. The policy adjustment to augment economic growth should promote through major changes in economic policies. The policy planning should be formulated keeping medium to long-term time horizon in mind, rather than on ad-hoc basis.

An expedient seven-point policy measure is, however, recommended for addressing the current and rising economic challenges. The seven-point policy measure comprises improved international diplomacy, employment enhancement strategies, higher revenue collection through expanding tax base, institutional reform in financial sector, increased private investment through incentivising investors, narrowing interest rate spread through effective harmonisation of macroeconomic policies, and development of a functional social security system.

Facets of Decelerated Growth and the Way Forward

| Nature of Declining Growth |

Trends of the Decline |

The Way Forward |

|

Unsatisfactory Investment |

Stagnation in savings and investment Decline in private investment | Expansion in investment in physical and social infrastructure rather than contraction |

|

Short- sightedness in Fiscal Management |

Low revenue collection Increasing public debt |

Expansion in net and areas of income tax such as property and wealth taxes

Reduction in consumption expenditure |

| Unfounded Adoption of Contractionary Monetary Policies | Falling private sector credit growth Crowding out of private investment High inflationary pressure |

Creative policy regime through the harmonisation of fiscal and monetary policies |

|

Disarrays in Real Sector |

Falling growth in agriculture Declining growth in manufacture Frequent

unreasonable hike in power tariff |

Increased investment in research and development and agricultural credit growth Increased incentives for setting up of manufacturing units Increased public investment in infrastructure |

|

Weak Performance in External Sector |

Decelerating growth of export

Decrease in the import of capital machinaeries Falling growth of remittance Irregularity in the inflows of FDI |

Diversification of exportable commodities instead of concentration in readymade garments

Provision of infrastructural facilities End of the current political uncertainties |

|

High Unemployment and Lower Decline in Poverty |

Increasing number of educated unemployed Possibility of current demographic dividend being missed

Decelerated decline in the incidence of poverty |

Increased incentives for expansion of productive capacity Adoption of employment enhancing pro-poor growth strategy |

Source: Adapted from Titumir and Rana (2014)

The aggregate demand has to be boosted up through the harmonisation of public and private investment. The policy of addressing structural issues rather than cyclical constraints could work better here. The fiscal policy needs to take a radical shift in the composition of the fiscal deficit from consumption to addressing supply-side bottlenecks through public investment in infrastructure. The increased public infrastructure investment will result in fiscal multipliers and crowd in private investment, unlike the current public consumption based fiscal deficit, which has been crowding out private investment demand. Output and employment gains may progressively move upward as private spending will not be crowded out, either by the upward pressure on interest rates arising from government credit demands or by the fears of eventual monetary accommodation and heightened inflation expectations which may accompany persistent deficits.

There is no alternative to increased revenue mobilisation to improve the fiscal balance of the country. First, the thrust of the tax reforms has to shift from the ad hocism to a structural one, comprising the principles of instituting progressive tax structure, avoidance of tax evasion and strengthening institutional capacity. For growth to continue the economy requires increased public expenditure in physical and socio- economic infrastructure. This is particularly required to have a structural shift from agriculture to industry and to service. Moreover, there is a need for an active fiscal policy with subsidies diverted towards the productive capacity and capability enhancing sectors.

Like the fiscal policy, the monetary policy of the country has to be harmonised to ensure a high investment ratio. Even if the central bank is assured that monetary pressure is causing the prices to go up, the central bank has to demonstrate its prudence by not resorting to across the board contraction of money supply rather choose a differential system to maintain the level of investment.

The exchange rate of the country has to be managed in such a way that exchange rate pass-through is kept at a minimal level and any sudden and unexpected ups and downs in the trade balance can be checked. In addition, the country has a few products for a few countries. An effective export diversification policy has therefore to be implemented through assisted monetary and fiscal measures. If expedient, prudent, context specific and creative policies are pursued, the economy would march forward and the country may soon graduate out of its least development status.

Reference

Mujeri K. Mustafa & Chowdhury T. Tahreen, 2014. Savings and Investment Estimates in Bangladesh: Some Issues and Perspectives in the Context of an Open Economy, June 2013.Dhaka: Bangladesh Institute of Development Studies. Available at: https://bids.org.bd/publication/DPaper/Dicussion_Paper_02.pdf

Bangladesh Bank. 2014, Major Economic Indicators. November, 2014. Dhaka, Bangladesh: Bangladesh Bank.

Bangladesh Bank. 2014, Monthly Economic Trend, November 2014. Dhaka, Bangladesh: Bangladesh Bank.

Bangladesh Bank. 2013, Selected indicators, December 2014. Dhaka, Bangladesh: Bangladesh Bank.

Ministry of Finance (MoF). 2014, Bangladesh Economic Review, 2014. Dhaka, Bangladesh: Finance Division, Ministry of Finance, Government of Bangladesh.

Unnayan Onneshan. 2014,Long On Realities, Short On Targets, Bangladesh Economic Update Volume 5, No.6, June 2014. Dhaka: Unnayan Onneshan. Available at: https://www.unnayan.org/reports/Budget/Budget_FY_2014-15/Budget_FY_2014-15.pdf

Unnayan Onneshan. 2014, Banking Sector Caught in Trap, Bangladesh Economic Update Volume 5, No. 7, July 2014. Dhaka: Unnayan Onneshan. Available at: https://www.unnayan.org/reports/meu/MEU_July_2014/MEU_July_2014.pdf

Unnayan Onneshan. 2014,Monetary Policy Statement (July-December, 2014): A Rapid Assessment, Bangladesh Economic Update Volume 5, No.8, August 2014. Dhaka: Unnayan Onneshan.Availableat:https://www.unnayan.org/reports/meu/MEU_August_2014/MEU_MPS_Au gust_2014.pdf

Unnayan Onneshan. 2014,External Sector: Current Trends, Bangladesh Economic Update Volume 5, No.10, September 2014. Dhaka: Unnayan Onneshan. Available at: https://www.unnayan.org/index.php/publications/all-publications/recent-articles

Unnayan Onneshan. 2014,Debt and Deficit: Recent Trends, Bangladesh Economic Update Volume 5, No.11, October 2014. Dhaka: Unnayan Onneshan. Available at: https://www.unnayan.org/reports/meu/Meu_October_2014/MEU_October_2014.pdf

Unnayan Onneshan. 2014,Energy Security: Recent Trends and Challenges, Bangladesh Economic Update Volume 5, No.12, November 2014. Dhaka: Unnayan Onneshan. Available at: https://www.unnayan.org/reports/meu/MEU_Nov_2014/MEU_Nov_2014.pdf

Unnayan Onneshan. 2012,Half Yearly Assessment of Economy of Bangladesh, Bangladesh Economic Update Volume 3, No.12, December 2014. Dhaka: Unnayan Onneshan. Available at: https://www.unnayan.org/index.php/publications/all-publications/recent-articles/86-half-yearly- assessment-of-the-economy-of-bangladesh

Unnayan Onneshan. 2013, Declining Growth: Mismathes in Fiscal and Monetary Management,Half Yearly Assessment of the Economy in Bangladesh, Bangladesh Economic Update Volume 5, No.11, October 2014. Dhaka: Unnayan Onneshan. Available at: https://www.unnayan.org/reports/meu/December%202013/Halfyearly%20assessment_Dec%2020 13.pdf

Prothom-alo, 2014. Countries Poverty is now at 25.6%, July28,2014. Available at: https://en.prothom-alo.com/bangladesh/news/51338/Country-s-poverty-rate-now-25.6%25

The Financial Express, 2014. Infrastructure and governance deficit Available at: https://www.thefinancialexpress- bd.com/old/index.php?ref=MjBfMDRfMjJfMTNfMV82XzE2NzEyMA

Appendix

Table: Scrap in loan

| Name of Company | Amount (taka) | Name of Branch & Bank |

|

Hall Mark |

2554 crore | Ruposhi Bangla branch of Sonali Bank |

|

Bismillah Group |

1100 crore |

Four private banks( Prime Bank, Jamuna Bank, Shahjalal Islami Bank |

|

BASIC Bank Limited |

1500 crore |

By Dilkusha, Gulshan and Shantinagar Branch |

| Imran Group | 101crore | Sholoshahar , Chittagong branch of Bangladesh Krishi Bank |

|

Director of Shahjalal Islami Bank limited |

140 crore |

Shahjalal Islami bank |

|

Ideal Cooperative society |

1000 crore | Directly from 70000 clients |

|

Destiny Group |

3800 crore | Directly from clients |

|

Paragon Group |

146.60 crore | Sonali bank |

|

T&Brothers |

609.9 crore | Sonali bank |

Source: The Daily star, April, September and July 2013,The New age,2012 The Daily Prothom-alo,July,2014

Bangladesh Economic Update is a monthly publication of the Economic Policy Unit of Unnayan Onneshan, a multidisciplinary research organisation based in Dhaka, Bangladesh. The report has been prepared by Nabila Nasrin. The Update has been copy edited by Abid Feroz Khan.

Address of UNNAYAN ONNESHAN

16/2 Indira Road, Farmgate Dhaka-1215, Bangladesh

Tel.: +880 (2) 58150684, +880 (2) 9110636

Fax: +880 (2) 58155804

Email: [email protected] Web: www.unnayan.org